Myths, monsters and curses in accounting education

Myths, monsters and curses in accounting education is based on a presentation by Paul Jennings and Toby York at the BAFA Accounting Education Special Interest Group conference in Durham, England, in May 2023.

The mythical monster

Original: Birmingham Museum and Art Gallery. Public domain.

In Greek mythology, the Minotaur was a violent, flesh-eating, half-bull and half-man. It was confined within a supposedly unsolvable underground labyrinth beneath the Cretan palace of Knossos. Every seven years, seven young men and women from Athens were despatched into the maze to feed the Minotaur.

Theseus, an Athenian prince, volunteered to navigate the labyrinth and slay the monster. Before entering, the King of Crete’s daughter, Ariadne, gave him a ball of thread — a clew — to trail behind him and, therefore, find his way out. Theseus successfully killed the Minotaur and escaped from the labyrinth.

He went on to desert Ariadne and indirectly caused his father’s suicide. So, he wasn’t an unmitigated hero, but for our purposes, the story’s point is his slaying of the Minotaur in the labyrinth. Or, more specifically, his (or Ariadne’s) successful strategy of focusing on the maze, not the monster.

The curse of knowledge

Of course, we’re not here to talk about the Greek myths but basic accounting — debits, credits, and financial statement elements. You’re probably an expert, so it’s unlikely we can tell you anything you don’t already know. You’ve, no doubt, been teaching these concepts successfully, some of you, for many years.

What we can tell you, however, is that experts acquire their knowledge mysteriously. They can perform at a high level without complete comprehension of what they’re doing or how they achieved their mastery. In our story, you might say they have a detailed understanding of the labyrinth, but it’s intuitive or implied knowledge.

Much of what experts do is invisible even to themselves.

Roger Kneebone Kneebone, R. (2020), Expert: Understanding the Path to Mastery. p. 6. London: Penguin Viking 1

In other words, experts don’t know what they do know. They’re so familiar with their expertise that they can no longer see the complexity of it. It’s become the way they see the world — it’s how the world works. So, they find it difficult to understand why non-experts can’t see what they see.

Michael Polanyi Polyani, M. (1958), Personal Knowledge: Towards a Post-Critical Philosophy. Chicago: University of Chicago Press 2 called this tacit knowing , often summarised as “we can know more than we can tell”. Ray Land and Jan Meyer Meyer, Jan H. F., and Ray Land. “Threshold Concepts and Troublesome Knowledge (2): Epistemological Considerations and a Conceptual Framework for Teaching and Learning.” Higher Education, vol. 49, no. 3, 2005, pp. 373–88. JSTOR, http://www.jstor.org/stable/25068074. Accessed: 16 May 2023 3 describe it in terms of threshold concepts. Once you cross a threshold, you experience a different way of knowing, and your previous struggles and difficulties immediately disappear. It’s somewhat related to the curse of knowledge. And like any curse, it’s not easy to dispel.

Educators, however, cannot afford the luxury of living under a curse. Your job requires you to pass on your expertise to others — a shift from you to them. It’s a relationship of care that requires you to think about your thinking. It requires you to break free of the curse of knowledge. This is harder than you might imagine, even if you successfully identify the sources of what Meyer and Land call troublesomeness and stuck places for students.

Debits and credits

When you learned the basics of accounting, maybe it was difficult, but you got there. You also accept that, to begin with, your students will struggle too. So you tell them to do the work, just as you did.

It’s a rite of passage, isn’t it? To slay the monster of debits and credits. Learn the rules. Use the tools. Debits on the left, credits on the right, DEAD CLIC York, T., (2021) “DEAD CLIC: it’s time to kill it off.” Accounting Cafe and T-accounts. These are our weapons of choice. We reassure students that if they use these often enough, they too will slay the monster, cross the threshold and become an expert.

But are we sending our students into a labyrinth with tools to kill a monster but no thread to help them navigate the maze? Like the Athenians who perished, we’re perhaps so focused on the monster that we neglect the maze. We might go further and say that the monster doesn’t exist. Because there’s no such thing as a debit, and there’s no such thing as a credit. Let us explain.

There are no such things as “debits” and “credits”

When you say debit or credit, what precisely do you mean? Surely, it depends. You might be referring to one or other of the sides of the accounting framework. We usually show the debit side on the left — and the credit side on the right. In this context, debit and credit refer to places or locations.

When considering transactions, each journal comprises debits and credits of equal amounts. These debits and credits affect or impact the accounting framework, which is an entirely different idea from debit and credit as locations.

So, we have locations and impacts. But there’s also a third aspect. We combine location and impact to record increases or decreases within the accounting framework. As you know, the rules are that a debit effect on the debit side increases amounts, as does a credit effect on the credit side. Conversely, a debit effect on the credit side and a credit effect on the debit side decrease amounts.

Doesn’t all this seem like a complicated way to introduce students to double entry? Well, yes, but that’s because it’s difficult to explain with words. As Don Moyer says succinctly, “If you’ve never seen a rhinoceros, a picture, not a paragraph, is what you need.”

But equally, skipping over the details also means failing to explain fully how accounting works. Your students will have an incomplete or incorrect schema of accounting fundamentals. Debits and credits are a threshold concept. And as we just described, the concept is about structure and relationships as much as language.

All knowledge has structure

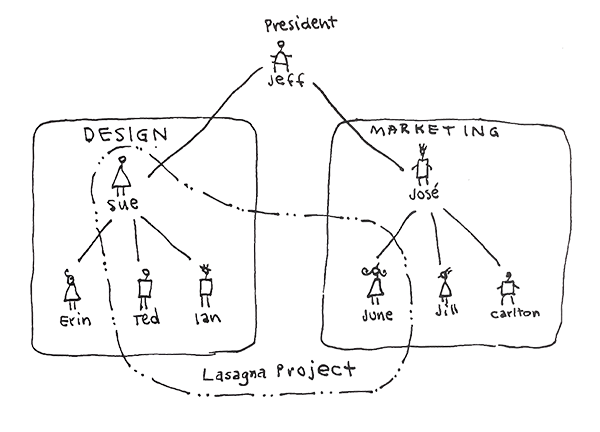

To illustrate the limits of explanations, Don Moyer Moyer D. (2010), The Napkin Sketch Workbook. ThoughtForm Inc. 4 sets out the “Lasagne Project” problem in The Napkin Sketch Workbook.

Jeff is the president of the company. Sue is the head of the Design team. Erin, Ted, and Ian work for Sue. José is the head of Marketing. June, Jill, and Carlton report to José. Sue, Ted, Ian, and June are working on the Lasagna Project.

Moyer then poses these somewhat challenging questions. Who’s the most senior person working on The Lasagne Project? Which department has more people allocated to the project? Who is not working on the project?

Try answering these questions before revealing the diagram below.

Reveal answer

The picture makes the questions trivially easy.

If we ask learners to rely solely on words, they find it difficult to extract meaning. It becomes much easier if they understand the knowledge structures. Sweller’s cognitive load theory does a good job of describing the problem from a neurological point of view, but we explore it here with a pedagogical lens.

Francis Miller Miller, F. (2018), Organising knowledge with multi-level content: making knowledge easier to understand, remember and communicate. Available at: https://www.francismiller.com/organising-knowledge/. Accessed: 12 March 2021 5 contends that concepts are made up of different elements structured to express meaning. So, “structure of knowledge” means the arrangement of knowledge elements and the relations between them. While we are specifically looking at financial statement elements, the principles apply to any kind of knowledge.

Structure is inherently spatial, so even if we explain knowledge structures explicitly, learners must use cognitive energy to convert our words into spatial structures. As experts, we may not even be aware of the structures which students are trying to work out implicitly.

Knowledge maps and multiple knowledge levels

The organisation of knowledge determines how readily the knowledge can be remembered, retrieved and extended beyond its original scope.

Instructional efforts need to pay as much attention to the organization of acquired knowledge as to its content.

Frederick Reif, quoted in Miller (2018)

In part, mastery requires moving between the whole and the underlying parts. This is what experts can do easily and quickly. As educators, our expression of how things work must replicate this. Learners struggle unnecessarily if the big picture is hidden in the details or if there is excessive focus on the details without seeing the big picture.

The solution is to provide explicit visual layouts of structures using multi-level knowledge maps. Reif used the analogy of geographical maps, starting from a map of the world and then increasing in detail right down to street maps. Google Maps does a great job of this so that we get the information we need as we zoom in and out.

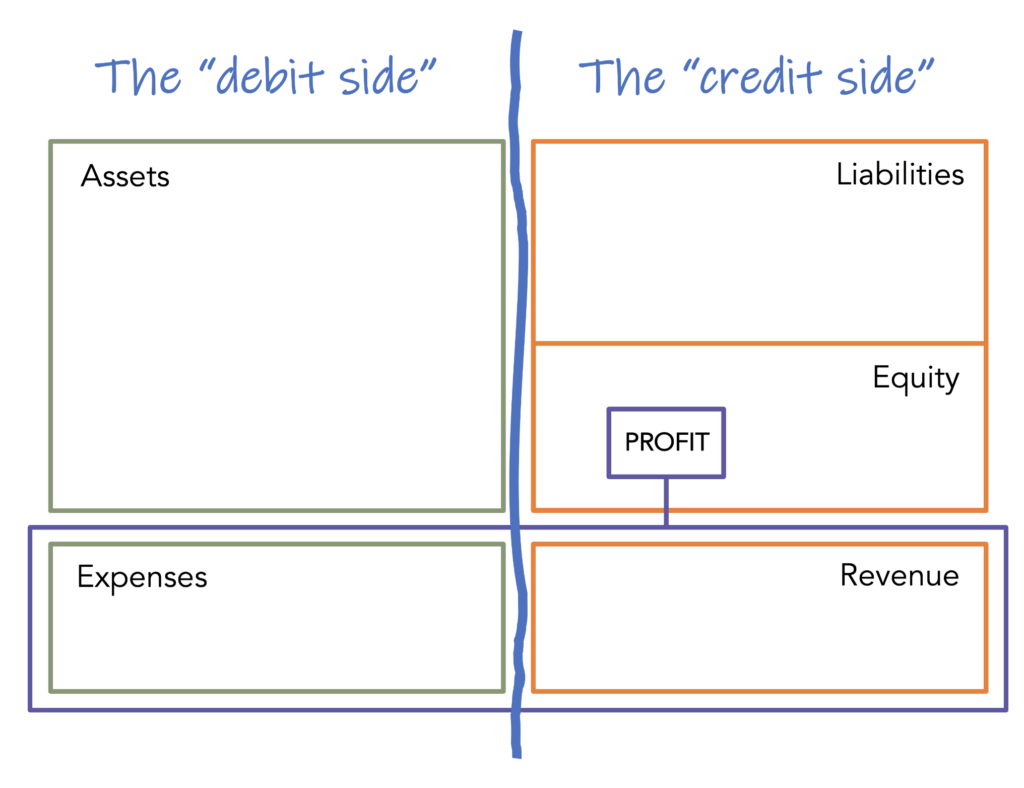

Colour Accounting makes knowledge structures visible

Colour Accounting is a unique approach to teaching accounting. Commercial trainers have been using it for over twenty years and academic institutions since the early 2010s. We believe it deserves to be more widely adopted.

It is consistent with established teaching practices such as the Socratic method and framework-based teaching endorsed by the IASB. It is not a naive or simplified version of the accounting framework. Still, it provides a comprehensive visual explanation of accounting on one page — the BaSIS Board — which is used in combination with colours to indicate debit-ness and credit-ness. Its secrets appear somewhat simplistic until you start using it.

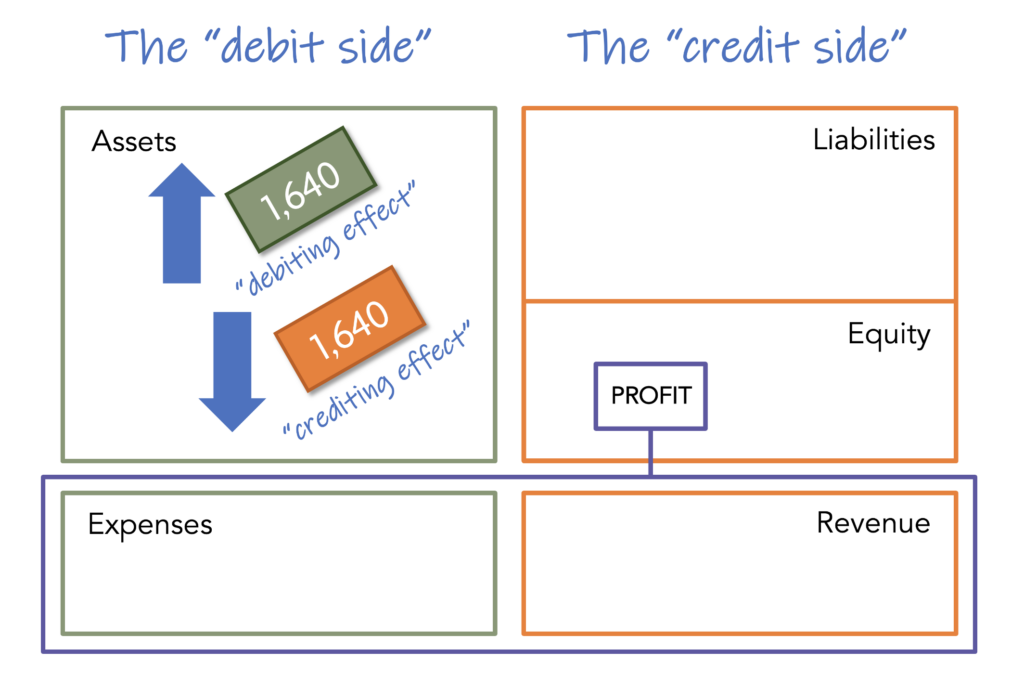

Debit and credit as location or place

On the accounting framework, the debit side is green, and the credit side is orange. The purple box around profit sits within equity. In a mechanical sense, revenue and expenses are “inside” the profit box. We use the analogy of double-clicking the profit box, revealing revenue and expenses. Understanding the relationship between equity and the statement of profit or loss is often an “a-ha” moment for learners.

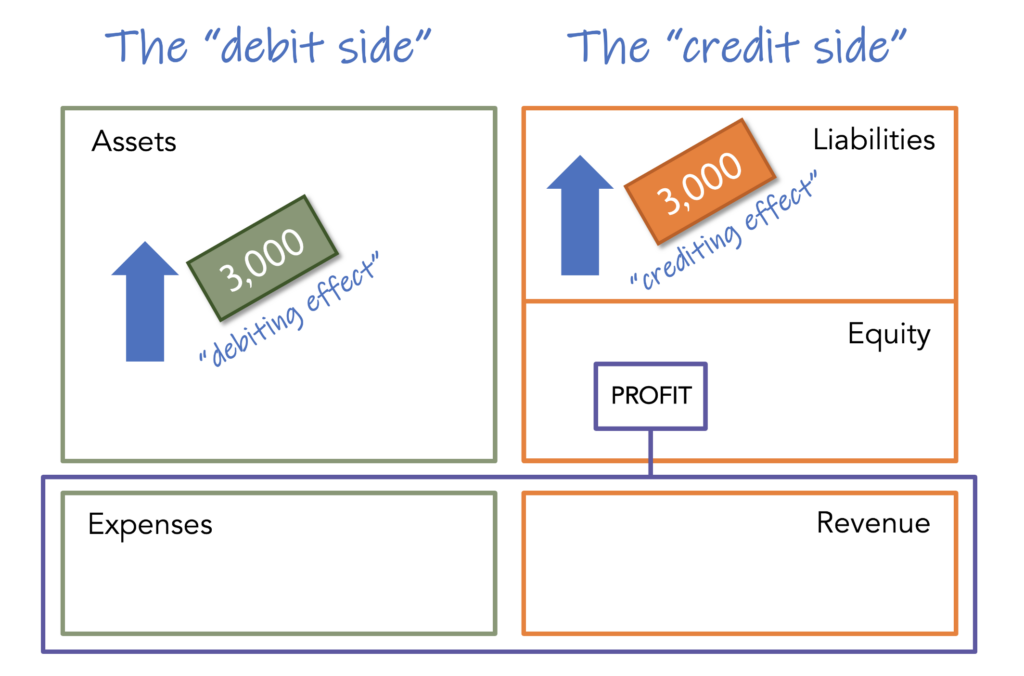

Debit and credit as effect or impact

Similarly coloured tickets represent debiting and crediting effects. In the physical version of Colour Accounting, students hold the tickets in their hands and decide where to place them on the BaSIS Board.

Placing a green ticket (debiting effect) on the green side (debit side) records an increase. Placing an orange ticket (crediting effect) on the orange side (credit side) also records an increase.

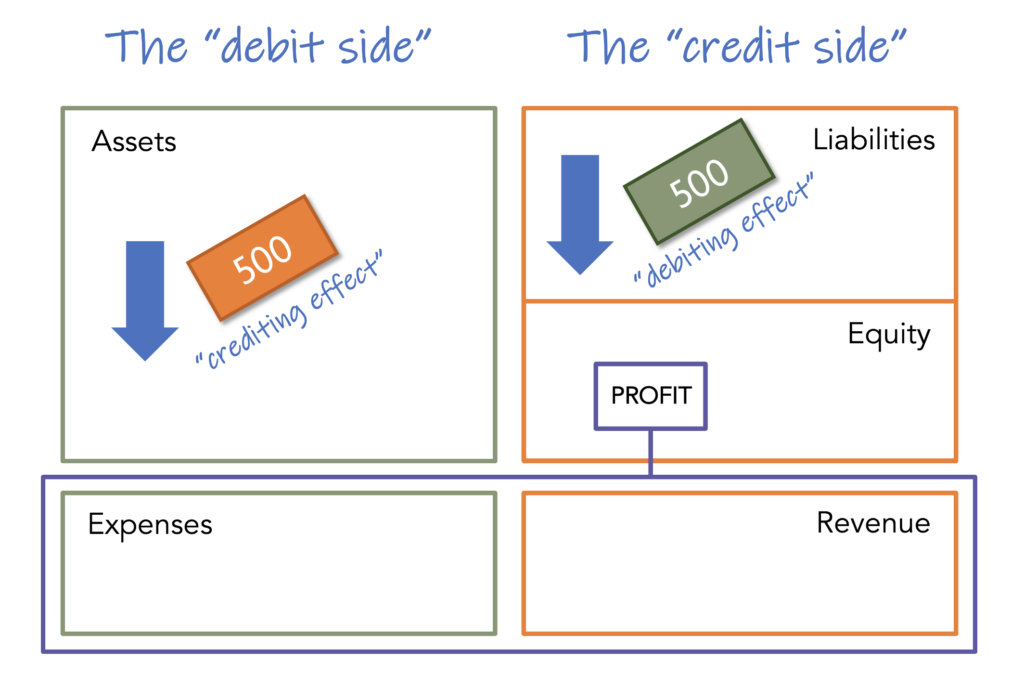

Placing the differently-coloured ticket on the accounting framework records decreases.

You can show students that placing both tickets on the same side is permitted, which is often overlooked in accounting texts and training manuals.

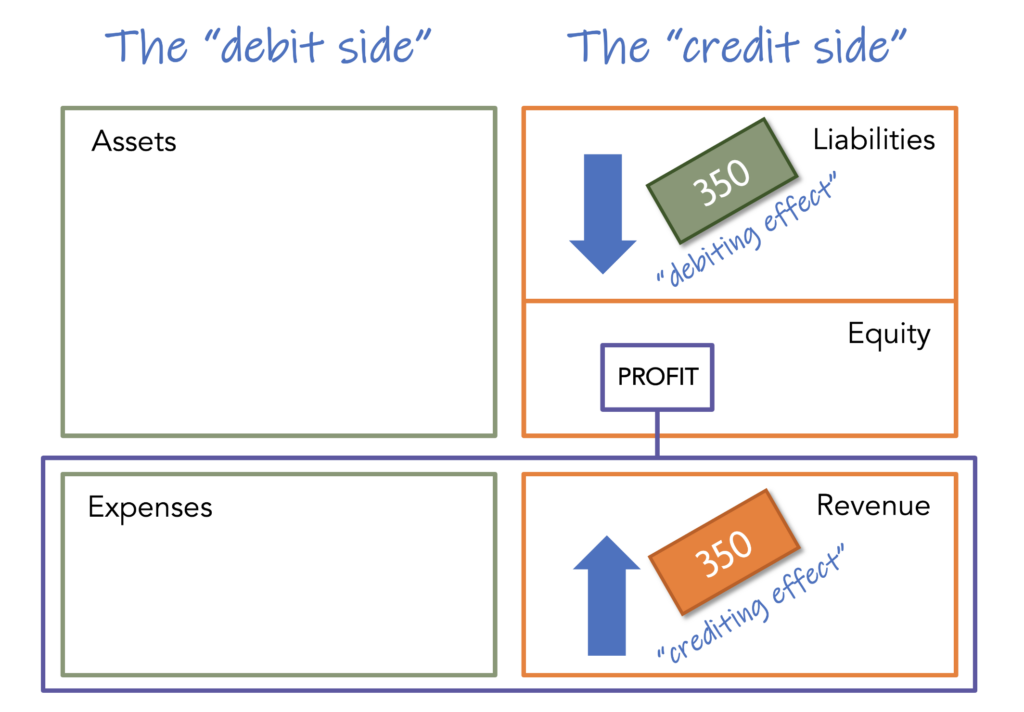

For completeness, here’s a transaction that increases revenue and decreases liabilities. In our experience, presented this way, students find what might be described as a complex transaction relatively straightforward. For example, the idea that deferred revenue (liabilities) is “released” to the statement of profit or loss (revenue).

It is clear that after each transaction, the accounting framework balances.

Extensive resources and applications exist to embed its use within an accounting degree programme. A growing body of accounting educators is developing class activities, online exercises and discussion cases that use Colour Accounting.

A short summary of the benefits

For educators, Colour Accounting helps you communicate more effectively, clearly and in an easier-to-understand format. It also improves one’s own thinking processes because using a multi-level knowledge map forces you to clarify the relationships between knowledge elements.

For learners, making knowledge structures explicit means that they don’t have to decipher implicit knowledge structures. They can use more of their energy on understanding, assessment and reflection. Structuring also helps memory. The big picture makes it easier to access subordinate knowledge associated with it.

Further considerations and research opportunities

The Pedagogy of Joy — Colour Accounting is fun and brings joy, energy and excitement into the learning environment. It may present an opportunity to stimulate a transformative attitude to learning accounting among students.

Physicality — Colour Accounting is learning by doing. It can also be delivered as a physical package that encourages independent exploration and debate while providing conceptually coherent understanding. It could provide an opportunity to explore the impact of active learning in an accounting education setting.

Left / right impairment — debit and credit are proxies for left and right. One of the reasons that Colour Accounting is effective is that it circumvents the requirement to hold “left and right” to understand of accounting.

Boundaries of accounting — the BaSIS Board’s contained structure makes the boundaries of current definitions and orthodoxy explicit. Why is there no sixth box? Why are certain assets not recognised? Why are retained earnings included within equity? Why is the residual described as “a claim of the investors”? What does the line between liabilities and equity mean?

Inclusion — anecdotally, students with dyslexia have reported perceived benefits of the Colour Accounting Learning System. The effects of Colour Accounting on inclusive education might be further investigated. In case you’re wondering, high-contrast materials are available for learners with colour-impaired vision.

Effectiveness — there is an opportunity to explore the effect of Colour Accounting on student learning. What are the effects of presenting threshold concepts in this way? Does it ritualise their knowledge or open them up to a deeper, more questioning mindset?

Resources, references and further reading

Download presentation: Myths, monsters and curses in accounting education (1.8MB PDF)

1 Kneebone, R. (2020), Expert: Understanding the Path to Mastery. p. 6. London: Penguin Viking

2 Polyani, M. (1958), Personal Knowledge: Towards a Post-Critical Philosophy. Chicago: University of Chicago Press.

3 Meyer, Jan H. F., and Ray Land. “Threshold Concepts and Troublesome Knowledge (2): Epistemological Considerations and a Conceptual Framework for Teaching and Learning.” Higher Education, vol. 49, no. 3, 2005, pp. 373–88. JSTOR, http://www.jstor.org/stable/25068074. Accessed: 16 May 2023.

4 Moyer D. (2010), The Napkin Sketch Workbook. ThoughtForm Inc.

5 Miller, F. (2018), Organising knowledge with multi-level content: making knowledge easier to understand, remember and communicate. Available at: https://www.francismiller.com/organising-knowledge/. Accessed: 12 March 2021.

York, T., (2021) “DEAD CLIC: it’s time to kill it off.” Accounting Cafe, 11 January, https://accountingcafe.org/2021/01/11/dead-clic/. Accessed: 30 April 2026

Wealthvox owns the intellectual property of the Colour Accounting Learning System and the BaSIS Board. Materials are available for non-profit educational use under Creative Commons. Contact Wealthvox for information.

© AccountingCafe.org

Part of the Pedagogy series

Join the Accounting Cafe community

How to cite this article: York, T. (2023) ‘Myths, monsters and curses in accounting education’, Accounting Cafe, 18 May. Available at: https://accountingcafe.org/2023/05/18/myths-monsters-and-curses/ (Accessed: [insert date])