Students need to understand that accounting is political

You may not think that accounting is political or that accountants should meddle in economics and politics. After all, their job is to report objectively on the performance and condition of corporations. Faithful representation, as we know, requires neutrality.

Corporations, however, are social inventions and financial reports are never passive accounts. They are stories that shape and are shaped [1] by the political, economic, and social environment in which they are told. [2]

Just look at the changes being made to reporting requirements and standards in relation to environmental, social and governance (ESG) disclosures. These are important and significant but the legal and regulatory frameworks have not, so far, kept pace — ESG compliance largely depends on the oversight of shareholders and there’s a limit to what can be expected from them to promote the interests of others over their own.

In truth, financial accounting is based on an ideological belief that profit-seeking behaviour leads to increases in the collective prosperity of society as a whole. It is this belief that provides moral legitimacy to the generation of profit by corporations, and lies behind our commercial laws, regulations and teaching, succinctly summarised in the words of Milton Friedman:

There is one and only one social responsibility of business—to use its resources and engage in activities designed to increase its profits so long as it stays within the rules of the game. [3]

Maybe there’s no space in the curriculum to accommodate a wide-ranging discussion of capitalism, but, with more modest ambition here are two related accounting principles—embedded within the US and international Conceptual Frameworks—that can be used to demonstrate the political nature of accounting in public interest entities (PIEs):

- Shareholders are owners of the corporation,

- with rights to its residual assets.

Disclosures of equity and retained earnings

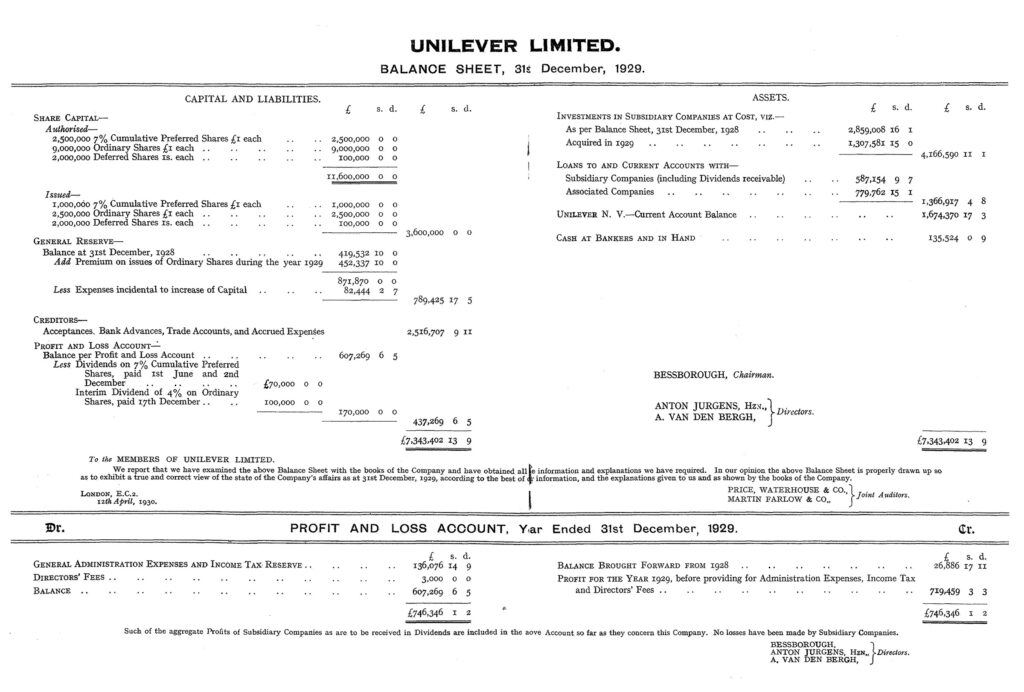

Before considering these rights of shareholders, look at the disclosure of capital and liabilities on Unilever’s balance sheet at 31 December 1929 and ask yourself, “To whom do the profits belong?”

OK, there are some peculiarities to our eyes: amounts are reported to the penny (£ s. d. is a reference to the UK’s pre-decimal system of pounds, shillings and pence), and capital and liabilities are on the left.

But of greater interest, the profit and loss account (retained earnings) is not specifically categorised as equity. To be clear, there were extensive shortcomings in financial reporting before the development of broadly enforced accounting standards and Generally Accepted Accounting Principles (GAAP) [Note 1], but whether intentional or not, this form of presentation avoids making an explicit statement about who has a claim to retained earnings.

The case for ownership: the proprietor view

Owners invest in a business enterprise with the expectation of obtaining a return on their investment… [4]

The claim that shareholders are owners of a corporation is consistent with economic theories that consider shareholders to be proprietors with rights to direct the corporation and to require it to act in their interests.

The proprietor view supports the idea that because shareholders own the company, then they indirectly own and/or have an exclusive claim on whatever the company owns. This, for the most part, is the ideological mask warn by accounting regulators, but it is contestable and the entity view of the corporation provides a partial alternative.

The case against ownership: the entity view

The entity view suggests that shareholders’ rights do not amount to ownership and therefore their claim is not to the residual assets. The arguments presented here are based in large part on the work of Dr Todd Sayre of the University of California [Note 2].

Firstly, parties other than shareholders compete legally and politically for rights to the residual assets. For example, the rights of workers through union negotiations, the rights of management who fight shareholders in takeover battles, and more recently the efforts to redefine the purpose of corporations by Business Roundtable in the US. [5] Even governments are not averse to asserting rights over and above their normal tax claims: in the UK energy companies, banks, and the technology sectors have been subjected to additional taxes as a result of generating “too much” profit.

Despite this, accounting regulators continue to privilege shareholders and lenders (and the ISSB’s draft sustainability standards [Note 3] indicate that they’re about to do so again).

Secondly, in law (and philosophy), ownership is determined by examining the bundle of rights held in relation to an asset, including rights of possession, use, disposal, abuse, and preventing others from accessing those assets.

Shareholders have no such rights in relation to a corporation’s assets or its net assets.

Ownership rights are usually accompanied by responsibilities but once called up share capital is paid, shareholders have no further liability for corporate debt or wrongdoings. [Note 4] Whatever rights shareholders have, they do not in the ordinary course of business come with responsibilities for the way that a company uses its assets.

Thirdly, a defining characteristic of limited liability entities is that they enjoy private ownership of their assets. If corporations are entities in their own right, then they are the rightful owners of their assets. In fact, the private ownership rights of entities prevent shareholders from extracting claims at will, which would be very disruptive to the corporation and possibly lead to its collapse.

In circumstances of debt default, creditors are able to access the assets of their debtors. If those assets include shares, creditors are only able to access the value of the rights represented within the shares, but cannot directly access a corporation’s assets or net assets. A powerful driving force behind limited liability legislation was to protect a corporation from the creditors of its investors. [6]

Fourthly, the right to vote in general meetings is sometimes cited as evidence of ownership rights, but this is not obvious. In other settings, such as workers’ voting rights on boards, or elections of school boards, local or state authorities or national governments, rights to vote are not indicative of ownership.

In its March 2022 Update [Note 5], the IFRS Interpretations Committee (IFRIC) declined to rule on whether a decision made by the shareholders is a decision of the entity, saying that it is an issue to be addressed in a future project.

Lastly, it is argued that even if shareholders do not have these rights directly, they have effective rights through control of management. This is somewhat true but is, in effect, limited to political influence, not control. Shareholders do not have a unified voice and their individual preferences differ.

Who has a claim on the residual?

The IFRS Conceptual Framework states “Equity claims are claims on the residual interest in the assets of the entity after deducting all its liabilities. In other words, they are claims against the entity that do not meet the definition of a liability.” The effect of this is that shareholders are the immediate beneficiaries from any failure to recognise obligations or potential obligations that do not meet the current recognition criteria for liabilities.

The environmental lobby, however, may be catching up. The Economist recently reported a case being brought by a Peruvian farmer against the German energy giant RWE “for belching nearly 7bn tonnes of greenhouse gases between 1854 and 2010” [7]. The case does not rely on applicable laws at the time—RWE polluted legally—but claims that the climate impacts of RWE’s actions were foreseeable and should have been mitigated. As The Economist says, the outcome of this case will have global implications.

You may not agree that these arguments are killer blows against the possibility that shareholders own the net assets, but it surely calls into question the basis for such claims. The very least we might say is that the tenets of accounting that assume ownership by shareholders are contestable.

© AccountingCafe.org

Notes

Note 1: Today, however, there is increasing concern that the accounting standard setting process has become unduly influenced by vested interests. On this topic, I recommend Karthik Ramanna’s “Political Standards: corporate interest, ideology, and leadership in the shaping of accounting rules for the market economy” (2015, The University of Chicago Press). There’s a wonderful, pithy remark on the sleeve from Larry Summers, former US Treasury Secretary: “…if war is too important to leave to generals, accounting is too important to leave to accountants”.

Note 2: Dr Todd Sayre presented a draft paper “Accountants are Helping to Destroy the World, but They Could Help to Save it” at an Accounting Cafe seminar in July 2021. It’s well worth watching: https://accountingcafe.org/2021/07/08/accountants-can-help-save-the-world/.

Note 3: The International Sustainability Standards Board (ISSB) has published the Exposure Draft IFRS S1 ‘General Requirements for Disclosure of Sustainability-related Financial Information (General Requirements Exposure Draft)’. It is consistent with previous IFRS publications by identifying the primary users of financial statements as “existing and potential investors, lenders and other creditors”.

https://www.ifrs.org/projects/work-plan/general-sustainability-related-disclosures/exposure-draft-and-comment-letters/

Note 4: Limited liability does actually have some limits. For example a dominant creditor may insist on the personal guarantees of shareholders, and the courts occasionally lift (or pierce) the veil of incorporation to hold shareholders personally liable for corporate debts. These exceptions invariably involve small or close companies and never large public corporations.

Note 5: Assessing whether a decision of shareholders is treated as a decision of the entity has been identified as one of the practice issues the International Accounting Standards Board (IASB) will address in its Financial Instruments with Characteristics of Equity (FICE) project.” IFRIC Update March 2022 Special Purpose Acquisition Companies (SPAC): Classification of Public Shares as Financial Liabilities or Equity (IAS 32 Financial Instruments: Presentation)—Agenda Paper 5: https://www.ifrs.org/news-and-events/updates/ifric/2022/ifric-update-march-2022/#3. This is the same project that might also review the conceptual distinctions between liabilities and equity.

References

[1] Hines, R. D. (1988) ‘Financial accounting: In communicating reality, we construct reality’. Accounting, Organizations and Society, Volume 13, Issue 3, 1988, Pages 251-261, Available at: https://doi.org/10.1016/0361-3682(88)90003-7

[2] Cooper, D. J. and Sheerer, M. J. (1984) ‘The value of corporate accounting reports: arguments for a political economy of accounting’. Accounting, Organizations and Society, Volume 9, No 3-4, Pages 207-232, University of Alberta School of Business Research Paper No. 2013-117, Available at: https://ssrn.com/abstract=2269177 (Accessed: 20 July 2022)

[3] Friedman, M. (1970) ‘A Friedman doctrine—the social responsibility of business is to increase its profits’. The New York Times, 13 September, Section SM page 17. Available at: https://www.nytimes.com/1970/09/13/archives/a-friedman-doctrine-the-social-responsibility-of-business-is-to.html (Accessed: 20 July 2022)

[4] FASB (2021) Conceptual Framework for Financial Reporting, Chapter 4, Elements of Financial Statements, Statement of Financial Accounting Concepts No. 8, paragraph E66. Available at: https://fasb.org/page/PageContent?pageId=/standards/concepts-statements.html (Accessed: 20 July 2022)

[5] Business Roundtable, Statement on the Purpose of a Corporation. Available at: https://opportunity.businessroundtable.org/ourcommitment/ (Accessed 29 June 2022)

[6] Hansmaan, H., Kraakman, R. And Squire, R. (2006) Law and the rise of the firm, Harvard Law Review, 119, March p.1335. Available at: https://heinonline.org/HOL/P?h=hein.journals/hlr119&i=1365 (Accessed: 20 July 2022)

[7] The Economist (2022), A Peruvian farmer takes on Germany’s largest electricity firm. The Economist, 2 June, online edition. Available at: https://www.economist.com/the-americas/02/a-peruvian-farmer-takes-on-germanys-largest-electricity-firm [subscription required] (Accessed 29 June 2022)

Thanks @Toby York for this insightful piece